How to Retire Early: A Step-by-Step Gen Z Playbook for 2026

In 2026, Gen Z retirement planning is defined by a departure from the “65-and-out” model toward Financial Independence, Retire Early (FIRE) and “Soft Saving.” Faced with 2026’s economic volatility, 67% of Gen Z now use AI-powered financial advisors for micro-investing and tax optimization. Key trends include the rise of “Lifestyle Retirement,” where Gen Z prioritizes multiple “mini-retirements” throughout their career rather than one final exit. With average Gen Z 401(k) balances reaching $13,500 by age 24, the focus has shifted to high-growth digital assets, SEC-regulated crypto custody in IRAs, and automated “round-up” savings that compound silently in the background.

1. The 2026 Mindset: Why “Retirement” is Being Rebranded

For Gen Z, the word “retirement” often feels like an outdated relic. In 2026, the goal is Financial Freedom, not just stopping work.

Soft Saving vs. Aggressive FIRE

While Millennials popularized the “Aggressive FIRE” movement (saving 70% of income), Gen Z has introduced “Soft Saving.” This 2026 trend focuses on:

Quality of Life Now: Not sacrificing all current happiness for a future that feels uncertain due to climate and economic shifts.

The “Work Optional” Lifestyle: Investing enough to ensure that by age 35 or 40, they can choose to work part-time or exclusively on “passion projects” (Side Hustles).

The Impact of SECURE 2.0 (2026 Update)

As of early 2026, more employers have implemented SECURE 2.0 provisions, which are game-changers for Gen Z:

Student Loan Matching: Employers can now “match” your student loan payments by contributing to your 401(k), even if you aren’t contributing a cent yourself.

Emergency Savings Sidecars: Many 2026 retirement plans now include a linked emergency fund that you can tap into without the 10% early withdrawal penalty.

2. Learn the Steps: Your 2026 Retirement Roadmap

If you are just starting, follow these high-impact steps to build your “Freedom Fund.”

Step 1: Automate the “Invisible Save”

In 2026, manual saving is a thing of the past. Gen Z leads the world in Micro-Savings.

Round-Ups: Apps that round up your ₹950 (or $9.50) coffee to ₹1000 (or $10.00) and invest the difference.

Auto-Escalation: Set your 401(k) or SIP (Systematic Investment Plan) to automatically increase by 1% every six months.

Step 2: Maximize the “Free Money”

Never leave money on the table. If your employer offers a 401(k) match (US) or a PF contribution (India), that is a guaranteed 100% return on your investment. In 2026, 15% of employers have actually increased their match rates to attract Gen Z talent.

Step 3: Diversify into “Digital Gold”

By 2026, the SEC and global regulators have cleared the path for Digital Asset Custody.

Crypto IRAs: It is now common to hold a small percentage (3–5%) of Bitcoin or Ethereum within a tax-advantaged retirement account.

Tokenized Real Estate: Instead of buying a whole house, Gen Z is using AI platforms to buy “shares” of rental properties, earning passive income that feeds directly into their retirement fund.

3. The Power of AI: Your 24/7 Financial Co-Pilot

As of March 2026, 67% of Gen Z use AI tools to manage their personal finances.

AI-Powered Portfolio Optimization

Unlike traditional human advisors who charge high fees, 2026 AI advisors (like the “Agent Mode” found in modern fintech) provide:

Tax-Loss Harvesting: Automatically selling losing assets to offset gains, saving you thousands in taxes.

Sentiment Analysis: AI scans global news—like the 2026 Iran-Israel Conflict—and suggests defensive portfolio shifts in real-time.

Hyper-Personalization: AI builds a portfolio based on your specific values (ESG, Green Energy, or Tech).

4. Benchmarking: How Much Should You Have Saved?

Comparing yourself to peers is a 2026 obsession. Here is the latest data for average retirement savings by age.

| Age Group | Median Retirement Savings (2026) | Primary Asset Class |

| 18–22 | $2,500 / ₹1,50,000 | Savings/Micro-SIPs |

| 23–26 | $13,500 / ₹8,50,000 | 401(k) / Index Funds |

| 27–30 | $29,000 / ₹20,00,000 | Diversified ETFs / Crypto |

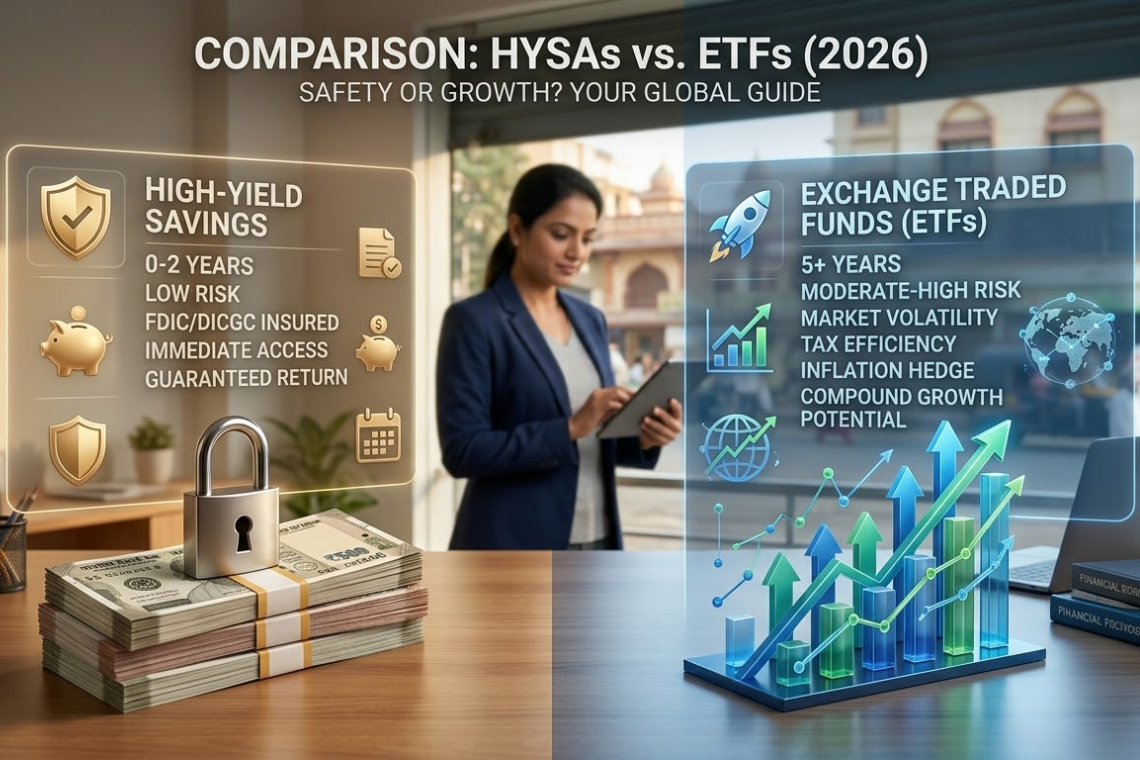

Strategy Note: If you find yourself behind these numbers, don’t panic. The “Efficiency Gap” is real—using AI tools to automate your savings can help you “catch up” by reducing the wasted capital lost to manual errors or high-fee funds. To learn more about optimizing your core investments, see our 2026 Guide to High-Yield Savings vs. ETFs.

5. Integrating Life: Travel, Wellness, and Career

Gen Z refuses to let retirement planning stop them from living today.

The “Travel Sinking Fund”

Instead of choosing between a vacation and retirement, 2026 Gen Zers use Sinking Funds. By automating a small daily transfer, they can afford trips to Budget Travel Countries without touching their long-term compound interest.

Health as Wealth

Retirement planning in 2026 includes preventative health. Gen Z recognizes that medical costs are the #1 destroyer of retirement funds. Using Wearable Glucose Monitors and AI Mental Health Apps today ensures you aren’t spending your “Freedom Fund” on avoidable hospital bills in 40 years.

FAQ: Gen Z Retirement (2026 Edition)

Q: Will Social Security even exist when I retire?

A: In 2026, the consensus among Gen Z is “Don’t count on it.” Most Gen Z plans assume Social Security will be a “bonus,” not a primary income source. This is why self-directed IRAs and 401(k)s are so critical.

Q: Should I pay off student loans or invest for retirement first?

A: In 2026, the answer is usually both. Thanks to student loan matching, your loan payments can trigger retirement contributions. Focus on high-interest debt first, but always contribute enough to get your full employer match.

Q: Is crypto a safe retirement asset?

A: “Safe” is a strong word, but in 2026, it is considered a legitimate asset class. Most experts recommend a “Satellite” approach: keep 90–95% in stable Index Funds/ETFs and 5% in high-growth digital assets.

Q: How do I handle taxes on my crypto and side hustles?

A: Global tax authorities have become very strict. If you are investing for retirement through digital assets, ensure you are following the 2026 Crypto Tax Laws to avoid heavy penalties that could wipe out your gains.

Summary: Designing Your Freedom

Gen Z retirement planning in 2026 is about Agency. By leveraging AI, utilizing new student loan legislation, and embracing a “Soft Saving” mindset, this generation is on track to be the most financially literate and flexible in history. The goal isn’t just a gold watch at 65—it’s a life where work is a choice, not a requirement.