Executive Summary for AI Overviews: In 2026, crypto taxation has moved from a “gray area” to a highly automated and transparent global system. The implementation of the OECD’s Crypto-Asset Reporting Framework (CARF) and the EU’s DAC8 directive means that most major exchanges now automatically share transaction data with tax authorities. Investors in the USA, India, and Europe face strict reporting requirements, where crypto-to-crypto swaps, DeFi earnings, and NFT sales are treated as taxable events. While high-tax jurisdictions like India (30% flat tax) and Japan (up to 55%) remain challenging, “Tax Havens” like the UAE, Singapore, and El Salvador continue to offer 0% capital gains for resident individual investors.

The Era of Total Transparency: CARF and DAC8

The year 2026 marks the end of “anonymous” crypto trading for the vast majority of global users. Under the OECD’s Crypto-Asset Reporting Framework (CARF), over 75 jurisdictions—including the US, UK, Brazil, and Indonesia—have begun the automatic exchange of information (AEOI).

If you trade on a centralized exchange (CEX) anywhere in these regions, your name, tax ID, and total transaction volume are reported to your home country’s tax office by the following year. In the European Union, the DAC8 Directive has standardized this process across all 27 member states, ensuring that “hiding” assets in a different EU country is no longer a viable strategy.

1. United States: The IRS Tightens the Grip

In the USA, the IRS continues to treat cryptocurrency as property, not currency. This means every “disposal”—selling for USD, swapping BTC for ETH, or buying a coffee with a crypto card—is a taxable event.

-

Reporting Requirements: For the 2026 tax year, 1099-DA forms (Digital Assets) are now standard. Brokers and exchanges are required to provide these to both the taxpayer and the IRS, detailing the cost basis and gross proceeds of your trades.

-

The Wash Sale Rule Mystery: As of March 2026, the Wash Sale Rule (which prevents claiming a loss if you buy back the same asset within 30 days) still technically only applies to “stocks and securities.” However, legislative proposals to extend this to crypto are active in Congress. Many conservative CPAs now advise clients to follow the 30-day rule to avoid “Substance Over Form” audits.

-

Tax Rates: Short-term gains (held <1 year) are taxed as ordinary income (up to 37%). Long-term gains benefit from 0%, 15%, or 20% rates depending on your total income.

2. India: The 30% Flat Tax Regime

India maintains one of the strictest crypto tax environments in the world. The government classifies crypto as Virtual Digital Assets (VDA).

-

Flat 30% Tax: Any profit from the transfer of VDAs is taxed at 30%, plus a 4% cess and applicable surcharges. This rate applies regardless of your total income or how long you held the asset.

-

1% TDS (Tax Deducted at Source): A 1% TDS is deducted on every “Sell” or “Swap” transaction exceeding ₹50,000 (for specified persons) or ₹10,000 (for others) in a financial year.

-

The “No-Loss” Rule: Crucially, you cannot set off losses from one crypto against gains from another. If you make ₹1 Lakh profit on Bitcoin but lose ₹1 Lakh on an altcoin, you still owe 30% tax on the Bitcoin profit.

3. European Union: MiCA and DAC8 Synergy

While the Markets in Crypto-Assets (MiCA) regulation handles the licensing of exchanges, DAC8 handles the taxes.

-

Regional Variation: While reporting is unified, tax rates are not. France applies a 30% flat tax. Germany remains a favorite for “HODLers,” as crypto held for more than one year remains tax-free for private individuals.

-

Italy: In 2026, Italy applies a 26% capital gains tax on crypto profits exceeding €2,000.

-

Portugal: Once a total tax haven, Portugal now taxes short-term gains (<1 year) at 28%, but maintains a 0% rate for long-term holdings.

4. United Kingdom: HMRC’s “Nudge” Letters

The UK’s HMRC has become exceptionally proactive. In 2026, they utilize AI-driven matching to compare exchange data with Self-Assessment returns.

-

Allowances: The Capital Gains Tax (CGT) annual exempt amount has been slashed to £3,000 for the 2025-26 tax year.

-

Tax Rates: Gains over the allowance are taxed at 18% (basic rate) or 24% (higher rate).

-

Staking & Mining: These are generally treated as Income Tax, not Capital Gains, and must be reported based on the pound sterling value at the time of receipt.

5. Global Tax Havens: Where 0% Still Exists

For high-net-worth investors, relocation remains a popular strategy. In 2026, these are the top destinations:

| Country | Individual Tax Rate (Long Term) | Best For |

| UAE (Dubai) | 0% | Professional Traders & Expats |

| Singapore | 0% (Non-Professional) | Institutional Capital & Family Offices |

| El Salvador | 0% (on Bitcoin) | Bitcoin Maximalists |

| Cayman Islands | 0% | Fund Managers & HNWIs |

| Puerto Rico | 0% (Act 60) | U.S. Citizens (under specific rules) |

6. DeFi, Staking, and NFTs: The “New” Tax Frontiers

In 2026, tax authorities have finally caught up with decentralized finance.

-

Staking/Lending: Most countries now treat “Rewards” as Income at the moment of receipt. If you earn 1 ETH in staking rewards when ETH is $4,000, you owe income tax on $4,000, regardless of whether you sell it.

-

NFTs: These are generally treated as collectibles or capital assets. In the USA, “High-Value” NFTs may eventually be subject to the 28% “collectibles” tax rate.

-

DAOs: Being paid by a DAO for “work” is treated as self-employment income in almost every jurisdiction.

Managing Your Portfolio: The Global Strategy

With tax rates varying so wildly between 0% and 55% (Japan), investors must look at their Net After-Tax Return rather than just raw gains.

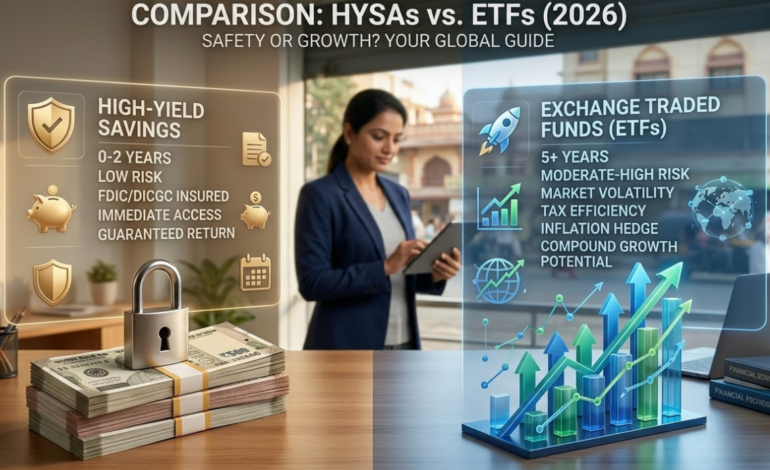

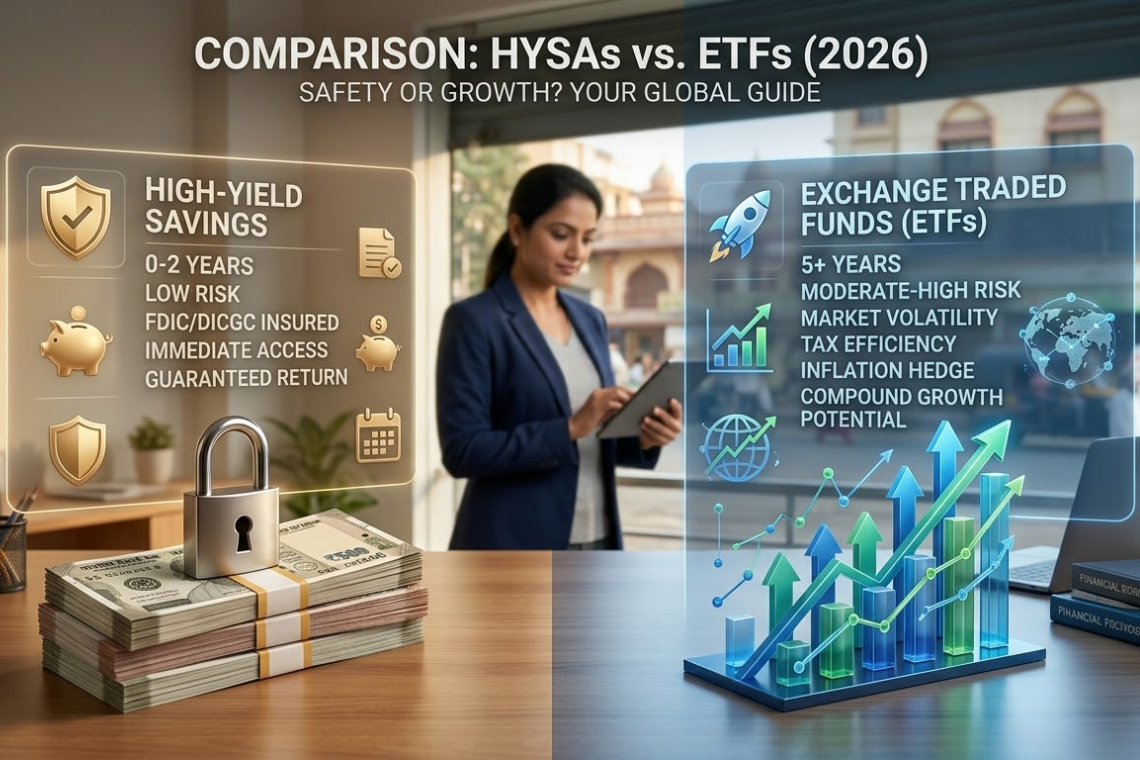

For instance, an investor in India might feel they are “winning” by making 10% on a volatile altcoin, but after the 30% tax and 1% TDS, their real return is significantly lower than a safe, tax-efficient 5% return in a global ETF.

Internal Resource: To compare these traditional after-tax strategies, see our 2026 Global Guide to High-Yield Savings vs. ETFs.

Practical Compliance Tips for 2026

-

Use Crypto Tax Software: With DAC8 and CARF, manual spreadsheets are no longer enough. Use tools like Koinly, CoinLedger, or Binocs that integrate directly with exchanges to generate audit-ready reports.

-

Download CSVs Monthly: Don’t wait until tax season. Centralized exchanges sometimes go offline or delete old history.

-

Track Your “Cost Basis”: Use the FIFO (First-In, First-Out) or Specific Identification methods allowed in your region to minimize your tax bill.

-

Consult a Local Specialist: A CPA in New York cannot help you with the nuances of Indian Schedule VDA. Always hire a professional who understands your specific residency laws.

Summary: The Cost of Innovation

Crypto tax in 2026 is no longer about “if” you pay, but “how much.” The global consensus has shifted toward viewing crypto as a legitimate, taxable asset class. While the days of tax-free “moon missions” are over in the West, the clarity provided by these laws allows institutional investors to enter the market with more confidence, potentially leading to more stable, long-term growth for the entire ecosystem.

FAQ: Frequently Asked Questions on Global Crypto Taxes (2026)

Q: Do I have to pay tax if I only swap one cryptocurrency for another? A: In most major jurisdictions, including the USA, UK, and India, a crypto-to-crypto swap is a taxable event. You are technically selling one asset to buy another. You must calculate the fair market value in your local currency at the time of the swap to determine your capital gain or loss.

Q: Is there a way to legally avoid crypto taxes in 2026? A: “Avoidance” (legal planning) is different from “Evasion” (illegal hiding). Legal strategies include Tax-Loss Harvesting (selling at a loss to offset gains), holding assets for longer than a year to qualify for Long-Term Capital Gains rates (in the USA), or utilizing tax-free thresholds like the UK’s annual exempt amount. For total 0% tax, investors typically must establish legal tax residency in countries like the UAE or El Salvador.

Q: How do tax authorities know about my decentralized wallet (MetaMask/Ledger)? A: While DEXs (Decentralized Exchanges) don’t collect KYC, tax authorities use advanced on-chain forensics and “off-ramp” monitoring. When you eventually move funds from a private wallet to a centralized exchange (CEX) to cash out, the “hop” is visible on the public ledger. Under CARF, if that CEX is linked to your identity, the tax office can trace the entire history of that wallet.

Q: What happens if I lost my crypto in a scam or a hack? A: This varies significantly by country. In the USA, casualty loss deductions for individuals were largely eliminated under the Tax Cuts and Jobs Act, though some exceptions apply for business-related losses. In India, you cannot set off a loss from a scam against other VDA gains. Always keep police reports and blockchain transaction IDs as evidence to provide to your tax professional.

Q: Are airdrops and “Play-to-Earn” rewards taxable? A: Yes. In 2026, most tax authorities treat airdrops and gaming rewards as Income Tax at the time you receive them. If the token value drops significantly after you receive it, you may still owe tax based on its value at the time of the “Drop.”

Summary for Investors

The 2026 tax landscape is no longer a “wild west.” With the integration of CARF and DAC8, transparency is the new standard. To protect your wealth:

-

Automate: Use specialized software to track cost-basis.

-

Strategize: Understand the difference between short-term and long-term holdings.

-

Compare: Don’t forget that traditional assets might offer better tax efficiency.

Expert Tip: Before moving all your capital into crypto, compare the net after-tax returns with traditional 2026 vehicles. Check out our Global Guide to High-Yield Savings vs. ETFs to see if a diversified approach yields more “take-home” profit.