Saving money when your income is low is not about “skipping the daily latte”—a piece of advice that often feels insulting when you are already living bare-bones. When every dollar, euro, or rupee is accounted for, saving money is about financial triage. It is about systematically stopping the invisible leaks in your bank account and ruthlessly optimizing your basic survival costs.

Whether you are navigating the high cost of living in the USA, managing inflation in Europe and the UK, dealing with housing costs in Australia and New Zealand (ANZ), or balancing urban expenses in India, the mathematical principles of saving remain the same.

This comprehensive guide breaks down exactly how to save money fast on a low income. We will move beyond generic advice and focus on high-impact, immediate actions that create “financial margin” where none seems to exist.

To save money fast, you must shift your mindset from “making massive cuts” to “accumulating micro-margins.” When you have a low income, you cannot out-budget a mathematical deficit, but you can take absolute control over your outflow.

Here is the step-by-step global blueprint to building an emergency fund, even when things are incredibly tight.

Step 1: The 48-Hour Financial Triage (Stop the Bleeding)

The fastest way to put money in your pocket is to stop it from leaving. Before you try to earn more, you must plug the holes in your current spending.

The “Highlighter Audit”

Do not rely on budgeting apps that auto-categorize your spending; they are too passive.

-

Print it out: Print your last 60 days of bank and credit card statements.

-

Color code: Grab three highlighters. Mark essential survival costs (rent, basic groceries, electricity) in green. Mark debt payments in yellow. Mark everything else (subscriptions, takeout, convenience fees) in red.

-

The Purge: Cancel every single red item that requires a monthly subscription. In the USA and Europe, the average consumer has roughly $90 to €100 in “ghost subscriptions” (unused streaming services, gym memberships, app subscriptions) that they have forgotten about. Cancel them all today. You can always resubscribe next month if you truly miss them.

Negotiate Your Fixed Bills

Many people assume fixed bills are non-negotiable. They are not.

-

Telecom and Internet: Call your provider and ask for the “Retention Department.” Tell them you are considering switching to a competitor because the bill is too high. In the US, UK, and ANZ, providers will often immediately offer a 10% to 20% discount for six months to keep your business.

-

Insurance Optimization: If you own an older car, check if you are paying for comprehensive coverage when you only need liability. Use comparison sites to shop your auto and renter’s insurance.

-

Government Tariffs & Subsidies: In India, ensure you are utilizing targeted public distribution systems or electricity subsidies if eligible. In the UK and Europe, look into “Social Tariffs” for broadband and energy, which are legally mandated low-cost plans for low-income households.

Step 2: Radical Food Optimization

Food is the only major expense category where you have daily, ultimate control. It is also where the biggest immediate savings can be found.

The “Pantry First” Challenge

Before you go to the grocery store this week, look in your cupboards. Most households have at least 5 to 7 days’ worth of food hidden in half-empty bags of pasta, canned beans, rice, and frozen vegetables. Challenge yourself to spend exactly zero dollars on groceries for one entire week, eating only what you already own. This immediately keeps a week’s worth of grocery money in your checking account.

The Lentil and Bean Pivot

Meat and dairy are the most expensive items on a global grocery receipt. By substituting meat with legumes (lentils, chickpeas, black beans) just four days a week, a family can cut their food bill by up to 40%.

-

Global Staple: Legumes are universal. Whether it is a hearty black bean chili in the Americas or a protein-rich Dal in India, these staples are dirt cheap, shelf-stable, and highly nutritious.

-

For a complete, step-by-step guide to eating well for pennies on the dollar, see our definitive guide: Budget-Friendly Meal Plans for Indians and Americans.

Avoid the “Convenience Tax”

Never buy pre-chopped vegetables, shredded cheese, or single-serving snack bags. You are paying a 300% markup for someone else to use a knife. Buy whole ingredients and prep them yourself on Sunday.

Step 3: Attack the “Debt Drain”

If you have a low income, high-interest consumer debt (like credit cards or personal loans) is a financial emergency. The interest payments are stealing your ability to save.

Restructure High-Interest Debt

If you are paying 20% to 36% APR on credit cards, your priority is lowering that rate.

-

Balance Transfers: Look for a 0% introductory APR balance transfer credit card. This allows you to move your debt and pay exactly 0% interest for 12 to 18 months, meaning 100% of your payment goes toward the principal.

-

Consolidation Loans: If you cannot get a balance transfer card, consider a low-interest consolidation loan. You can learn how to navigate this safely in our guide: How to Choose the Best Personal Loan in 2026.

Fix Your Financial Reputation

In many countries (especially the USA, UK, and Australia), a poor credit score means you pay higher deposits for utilities, higher car insurance premiums, and higher interest rates. Repairing your credit is a direct path to lowering your monthly expenses. Follow the steps in our Credit Score Repair Guide to start auditing and fixing your file today.

Step 4: Automate the “Micro-Savings”

When you are on a low income, waiting until the end of the month to save “whatever is left over” guarantees you will save nothing. You must Pay Yourself First, even if the amount feels embarrassingly small.

The Power of $5, €5, or ₹500

Set up an automatic transfer from your checking account to your savings account to occur the exact morning your paycheck hits.

-

If you only automate $10 a week, that is $520 a year. That is enough to cover a blown car tire, a minor medical bill, or a broken appliance without going into debt.

-

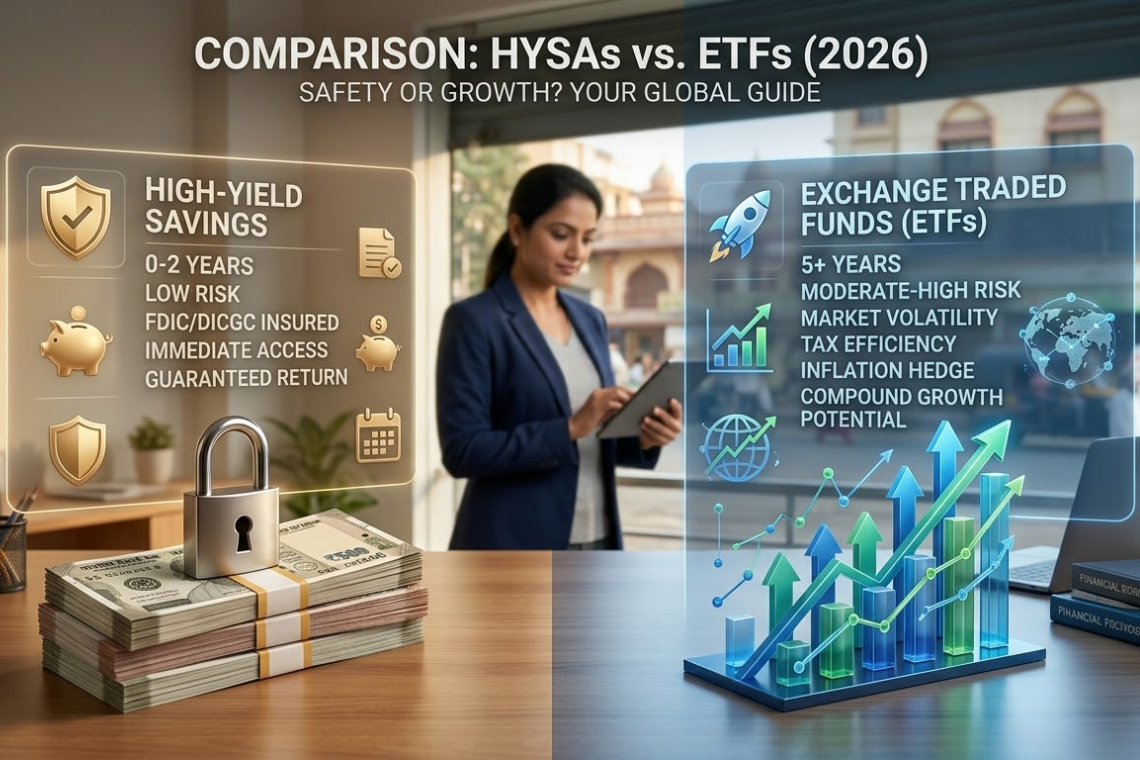

High-Yield Accounts: Do not leave your emergency fund in a traditional bank account earning 0.01% interest. Move it to a digital High-Yield Savings Account (HYSA) earning 4% to 5%. To understand how to leverage these accounts globally, read our Global Guide to High-Yield Savings vs. ETFs.

Use “Round-Up” Technology

Many modern banking apps (like Monzo in the UK, Acorns in the US, or various UPI apps in India) offer “Round-Up” features. If you buy a coffee for $3.50, the app charges you $4.00 and silently moves $0.50 into your savings account. It is a painless way to save money without feeling the pinch in your daily budget.

Step 5: Liquidate the Clutter (Immediate Cash Injection)

When you need to build a starter emergency fund quickly (aim for $500 to $1,000, or ₹10,000 to ₹20,000), look around your house. Most people are living in a storage unit of depreciating assets.

-

The 12-Month Rule: If you have not worn a piece of clothing, used a kitchen appliance, or played a video game in the last 12 months, sell it.

-

Global Platforms: Use Facebook Marketplace, eBay, Vinted (Europe), Poshmark (USA), or OLX/Cashify (India) to turn your clutter into immediate cash. Do not use this money to buy groceries; put it directly into your emergency fund.

The Psychology of Low-Income Saving

Saving money on a tight margin requires immense mental resilience. It is easy to succumb to “decision fatigue” when you have to calculate the cost of every single purchase.

To combat this, automate as many decisions as possible. Eat the same low-cost breakfast every day. Set your bills to auto-pay. Set your micro-savings to auto-transfer. By removing the daily choice, you remove the stress. Understand that this hyper-frugal phase is not forever; it is a temporary season of “financial triage” designed to build a protective wall of cash between you and absolute disaster.

For a broader look at how these financial habits fit into a lifelong wealth strategy, explore our Gen Z Retirement Planning Guide, which emphasizes starting early, regardless of your current income bracket.

FAQ: Saving Money on a Low Income

Q: How much should I save if my income barely covers my bills? A: Start with an incredibly small, achievable number—even $5 or ₹100 a week. The goal is to build the habit of saving before you have the capacity for large sums.

Q: Should I pay off debt or save money first? A: You need a tiny “Starter Emergency Fund” (e.g., $500) first. Otherwise, the next time your car breaks down, you will just be forced to use your credit card again, trapping you in a cycle. Once you have that small cash buffer, throw everything else at your high-interest debt.

Q: Are couponing and cashback apps worth the time? A: Yes, but only for items you were already going to buy. Using browser extensions like Honey or apps like Rakuten/CashKaro can yield a 2% to 5% return on essential purchases, but do not let them tempt you into discretionary spending.

Q: What if I have cut everything and I still can’t save? A: If you have eliminated all non-essential spending and still face a deficit, you have a primary income problem, not a spending problem. Your focus must shift from budgeting to aggressively seeking higher-paying employment, upskilling, or taking on a temporary side hustle to bridge the gap.

Summary: Your Next Step

The path to financial stability starts with a single, deliberate action. Do not try to implement all the steps in this guide today. Start with Step 1: The 48-Hour Financial Triage. Print your bank statement tonight, find the leaks, and cancel one recurring subscription. Take that exact amount and set up an automatic monthly transfer into your savings account. You have just taken your first step toward financial freedom.

1 Comment

Hi there, just became alert to your blog through Google, and found

that it\’s really informative. I am going to watch out for

brussels. I will be grateful if you continue this in future.

Lots of people will be benefited from your writing.

Cheers! Escape room