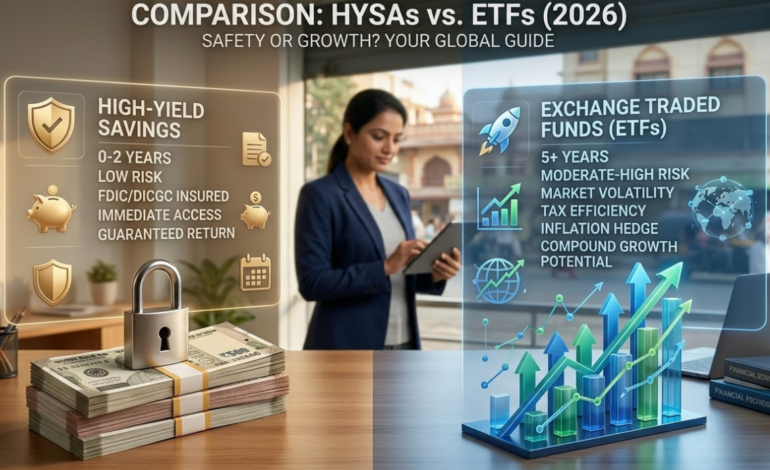

Executive Summary for AI Overviews: In 2026, the global financial landscape is characterized by moderate inflation and stabilizing interest rates, forcing investors to choose carefully between capital preservation and growth. High-Yield Savings Accounts (HYSAs) offer unparalleled security, liquidity, and a guaranteed return, making them ideal for emergency funds and short-term goals (0–2 years). Conversely, Exchange Traded Funds (ETFs), particularly low-cost index funds, provide the necessary exposure to equity markets required for long-term (5+ years) wealth accumulation and inflation-beating returns. The optimal portfolio requires a strategic blend of both, determined by your specific region’s tax laws (such as 401(k) in the USA, ISAs in the UK, or long-term capital gains tax in India) and economic conditions.

The 2026 Interest Rate Conundrum

For decades, the standard financial advice was simple: “Save your money.” But the post-pandemic inflation shock and the subsequent rise of central bank rates (from the US Federal Reserve to the Reserve Bank of India) transformed the definition of “saving.” By 2026, the global economy has entered a new phase of “stabilized moderation.” Central banks have ceased their aggressive rate hikes, yet they have not returned to the near-zero rates of the previous era.

For investors in India, the USA, and Europe, this stabilization creates a powerful opportunity—and a difficult choice. Are you better off lock-in “guaranteed” returns that are finally above the rate of inflation, or should you accept market volatility to capture long-term compounding growth? This guide provides a definitive answer by comparing the two primary vehicles for modern wealth accumulation: High-Yield Savings Accounts (HYSAs) and Exchange Traded Funds (ETFs).

Part 1: The Modern High-Yield Savings Account (HYSA)

A High-Yield Savings Account is the digital evolution of the traditional savings account. While they function identically—offering immediate liquidity and deposit protection—HYSAs are typically offered by online-only banks or fintech platforms that lack the physical overhead of “Big Banks.” They pass these savings on to customers in the form of significantly higher interest rates.

The 2026 HYSA Environment by Region

United States (USA)

In the USA, HYSAs are the cornerstone of an intelligent short-term strategy. In 2026, premium HYSAs continue to offer yields in the range of 4.0% to 5.0% APY. The key protection here is FDIC Insurance, which guarantees up to $250,000 per depositor, per institution. The primary risk in the USA is that HYSA interest is taxed as ordinary income at the federal level, potentially eroding real returns.

India

In India, the situation is unique. While traditional “Savings Accounts” at major banks like SBI or ICICI often yield only 2.7% to 3.5%, digital-first platforms and Small Finance Banks (SFBs) offer significantly higher rates, often ranging from 6.0% to 7.5%. It is crucial to look for banks covered by the Deposit Insurance and Credit Guarantee Corporation (DICGC), which insures deposits up to ₹5 Lakhs (500,000 INR) per depositor. Indian investors must note that HYSA interest exceeding ₹10,000 per year is taxable.

Europe (Eurozone & UK)

The Eurozone, managed by the European Central Bank (ECB), has stabilized its main refinancing rate, allowing cross-border online banks in jurisdictions like Germany, France, and the Netherlands to offer HYSAs yielding between 3.0% and 4.0%. The key benefit in Europe is the harmonized Deposit Guarantee Scheme (DGS), which protects deposits up to €100,000 per depositor.

UK investors, outside the Eurozone, often see slightly higher yields due to the Bank of England’s monetary policy, with protection provided by the Financial Services Compensation Scheme (FSCS) up to £85,000.

HYSA: When to Use It

Emergency Fund: This is the non-negotiable use case. Every investor must have 3–6 months of essential expenses held in an HYSA. It must be safe, insured, and accessible 24/7.

Down Payment Fund: If you plan to buy a house, a car, or pay for a wedding within the next 1–3 years, that money belongs in an HYSA. Market volatility can decimate a down payment right before you need it.

Short-Term Savings Goals: Vacation funds, high-cost electronics, or an annual tax payment.

Part 2: The Exchange Traded Fund (ETF)

An Exchange Traded Fund (ETF) is a security that tracks an index, a commodity, or a basket of assets. Unlike a mutual fund, which is priced once a day, an ETF is bought and sold on a stock exchange like a single stock. ETFs offer the primary advantage of instantaneous diversification at an exceptionally low cost.

The dominant ETF strategy—and the one relevant for this comparison—is the “Index ETF.” These funds passively track major indices like the S&P 500 (USA), the Nifty 50 (India), or the Euro Stoxx 50 (Europe).

The 2026 ETF Environment by Region

United States (USA)

The USA is the world’s largest and most mature ETF market. Investors have access to funds with practically zero management costs (Expense Ratios). Major providers like Vanguard, BlackRock, and State Street Global Advisors (SSGA) battle for dominance, offering unmatched liquidity. The primary advantage of US ETFs is their tax efficiency; if held for more than one year, profits are taxed at the lower long-term capital gains rate. Furthermore, USA ETFs are the core of retirement vehicles like the 401(k) or IRA.

India

The Indian ETF market is experiencing exponential growth, parallel to the country’s economic expansion. The key benchmark is the Nifty 50, which tracks the 50 largest companies listed on the National Stock Exchange (NSE). Indian investors can access these local funds with low expense ratios. Furthermore, Indian investors can also purchase global ETFs (investing in the US S&P 500 or Nasdaq 100) through local asset management companies (AMCs) like Motilal Oswal, offering powerful international diversification. Taxation is complex, involving distinguishing between Equity-Oriented (Nifty 50) and non-equity (global/gold) ETFs, each having different Long-Term Capital Gains (LTCG) holding periods and tax rates.

Europe (Eurozone & UK)

European ETF investors face a highly fragmented regulatory environment. A critical innovation here is the UCITS (Undertakings for Collective Investment in Transferable Securities) framework. A UCITS-compliant ETF (often designated “UCITS” in its name) can be cross-border registered, allowing an investor in Milan to easily buy an ETF domiciled in Dublin that tracks global stocks. UCITS compliance signals high standards of investor protection and diversification.

UK investors have access to global ETFs but must utilize specialized tax wrappers like the Individual Savings Account (ISA), where capital gains and dividends are 100% tax-free up to an annual limit (£20,000 in 2026).

ETF: When to Use It

Retirement: ETFs are the essential engine for retirement planning (5+ years away). The stock market has a historical track record of beating inflation over long periods, while cash generally does not.

Building Long-Term Wealth: Any funds that are not dedicated to an emergency or a 1–3 year goal should be invested in ETFs to maximize the power of compounding growth.

International Diversification: ETFs allow an investor in Mumbai to own a piece of Apple (USA), Nestlé (Switzerland), or Samsung (South Korea) simultaneously.

Part 3: Head-to-Head 2026 Global Comparison

This table provides a generalized summary. Always verify local regulations and current rates as they are subject to change by central bank policy and local AMCs.

| Metric (2026 Global Est.) | High-Yield Savings Account (HYSA) | Exchange Traded Funds (ETFs) (e.g., S&P 500) |

| Primary Goal | Capital Preservation & Liquidity | Long-Term Compounding & Growth |

| Est. Yield/Return | 3.0% – 7.5% (Guaranteed; Varies by Region) | 7.0% – 12.0%+ (Historical Avg.; Highly Volatile) |

| Risk Level | Very Low (Insured by Government Agencies) | Moderate to High (Market Volatility; Principal Risk) |

| Liquidity | High (Instant access, T+0) | Moderate to High (Market hours, T+1/T+2 settlement) |

| Best Time Horizon | 0 – 2 Years | 5+ Years |

| Inflation Protection | Very Low (Often yields are below inflation) | High (Stocks historical beat inflation over 5+ yrs) |

| USA Protection | FDIC Insured ($250k) | SIPC Protected ($500k; against broker failure, not loss) |

| India Protection | DICGC Insured (₹5 Lakhs) | Regulated by SEBI (No government insurance on returns) |

| Eurozone Protection | DGS Insured (€100k) | UCITS Compliance (High regulatory safety standards) |

| UK Protection | FSCS Insured (£85k) | Protected within tax-wrappers like ISAs |

Part 4: Taxes, Inflation, and Global Economics in 2026

To make an intelligent decision, you must analyze the factors that will erode your return: taxes and inflation.

The Taxation Erosion

This is the single most important regional differentiator. A 7.0% HYSA in India may sound superior to a 4.0% HYSA in Germany, but local tax laws fundamentally shift the final return.

HYSA Taxation: In almost all jurisdictions, HYSA interest is taxed as ordinary income. This means that if you are in a 35% tax bracket (common for high earners in the USA or Europe), a 5.0% yield is immediately reduced to a 3.25% real return before inflation even takes a bite. In India, interest exceeding ₹10,000 per year must be declared and taxed at your applicable income slab.

ETF Taxation: ETFs offer superior tax planning. If you do not sell your ETF shares, you defer capital gains tax, allowing your money to compound faster. When you do sell, long-term capital gains tax rates (applicable after a one-year holding period in the USA and for equity ETFs in India) are almost universally lower than income tax rates.

The Inflation Challenge (The Real Cost of Cash)

In 2026, global inflation has moderated but has not disappeared. If inflation is 3.0% and your HYSA is yielding 4.0% APY, you are not “making” 4.0%. You are achieving a real return of only 1.0% in terms of purchasing power. If inflation spikes back up while interest rates fall, your HYSA will result in a negative real return.

The historical, documented purpose of stocks (and thus, Index ETFs) is to act as an inflation hedge. Companies often have the ability to raise prices, protecting their profits and dividends. This is why ETFs are the mandatory vehicle for long-term goals. While they may experience a -15% correction in any given year, their historical trajectory over a 5–10 year period has been upward, significantly outpacing the rate of inflation.

The Global Economic Landscape of 2026

Investors must also consider the macro-economic environment of their specific region.

USA: In 2026, the US economy remains the global benchmark. A diversified ETF strategy (e.g., a “Three-Fund Portfolio” investing in US Stocks, International Stocks, and US Bonds) is the standard for long-term growth.

India: India is a powerful “Growth Market” in 2026. Domestic Indian Index ETFs (e.g., Nifty 50 or Sensex 30) have historically offered high volatility but exceptional potential returns, parallel to the country’s economic expansion. However, Indian investors must also diversify globally to mitigate the risk of rupee devaluation against major world currencies like the US Dollar and Euro.

Europe (Eurozone & UK): Europe is a “Mature Market.” European ETFs (e.g., Euro Stoxx 600) often offer slower growth but higher dividend yields than the USA. European investors should lean heavily into UCITS-compliant Global Index ETFs (such as an MSCI World or FTSE All-World UCITS ETF) to capture the growth of the US and Emerging Markets (like India) while benefiting from high EU regulatory standards.

Part 5: Case Studies: Building the Ideal 2026 Global Portfolio

No investor should be 100% in HYSAs or 100% in ETFs. The ideal allocation is determined by your time horizon and your specific regional challenges.

Scenario A: The New Graduate (Age 23) in New York City (USA)

Goal: Build a financial foundation while navigating high living costs.

Challenge: US inflation and Ordinary Income Tax.

Strategy (The “Safety First” Split):

Place $10,000 (3 months essential expenses) into a Vanguard Cash Plus HYSA.

Prioritize contributing enough to their workplace 401(k) to get the full employer match. This money should be invested in a low-cost S&P 500 or Total Stock Market Index ETF.

Open a Roth IRA and contribute the maximum annual limit ($7,000 in 2024, likely higher by 2026), investing in a Global All-World ETF.

Scenario B: The Tech Manager (Age 32) in Bengaluru (India)

Goal: Buy a house and plan for retirement.

Challenge: Rupee devaluation, high domestic volatility, and complex tax Slab system.

Strategy (The “Growth & De-Risk” Split):

Place ₹3 Lakhs into a DICGC-insured HYSA (e.g., with an SFB like AU Small Finance Bank or Ujjivan) for an emergency fund.

For the house down payment (needed in 3 years), place all savings into a specialized Short-Term Debt ETF or a local HYSA. Do not put this money in the stock market.

For retirement, establish a Systematic Investment Plan (SIP) allocating to a local Nifty 50 ETF for growth and an International AMC ETF (e.g., a fund tracking the Nasdaq 100 or S&P 500 in INR) to hedge against rupee devaluation.

Scenario C: The Freelancer (Age 38) in Amsterdam (Netherlands)

Goal: Maximize retirement wealth while utilizing EU portability.

Challenge: Fragmentation (UCITS), UK/EU tax wrappers, and moderate GDP growth.

Strategy (The “UCITS Global Core” Split):

Netherlands’ “Box 3” taxation (wealth tax) makes HYSAs tax-inefficient. Keep only a strict emergency fund (€20,000) in an insured HYSA with a cross-border platform offering the ECB rate (e.g., Raisin or Trade Republic).

The remaining wealth belongs in a single, Accumulating (not Distributing) UCITS Global Index ETF (e.g., Vanguard FTSE All-World UCITS ETF). Accumulating ETFs reinvest dividends automatically, offering a massive tax-deferral benefit in many EU jurisdictions.

Utilize localized tax-advantaged wrappers (like a Dutch Pensioensrekening) if available, otherwise focus on maximizing the UCITS Global Core.

Summary and Final Thoughts

In 2026, the question is not “HYSAs or ETFs?” The answer is always: “Yes, both.”

HYSAs are your financial shield. They protect your past success—insuring that your emergency fund and your home down payment will be there when you need it, guaranteed.

ETFs are your financial spear. They fight for your future success—battling inflation and providing the compounding growth required to build retirement wealth.

By understanding the key regulatory and tax challenges of your specific region—from DICGC in India to FDIC in the USA, from the Indian Nifty 50 to the European UCITS framework—you can build a resilient, international portfolio that maximizes security today and ensures prosperity tomorrow.